Global Copper Smelting Faces Crisis as Treatment Fees Plunge Below Zero

October 15, 2025

Copper smelters worldwide are facing a crisis as declining treatment and refining charges (TC/RCs) push fees into negative territory, with the benchmark index dropping to -$66.60 per tonne, threatening the sustainability of operations.

This crisis is driven by a supply-demand imbalance, with expanding smelting capacity—especially in China—and stagnant mine production leading to a projected concentrate supply deficit of around 500,000 tonnes by 2026.

Chinese smelters, controlling about 60-65 facilities, continue to operate at high capacity despite negative margins, which hampers market rebalancing and prolongs the crisis, especially as Chinese capacity expands and reduces reliance on imports.

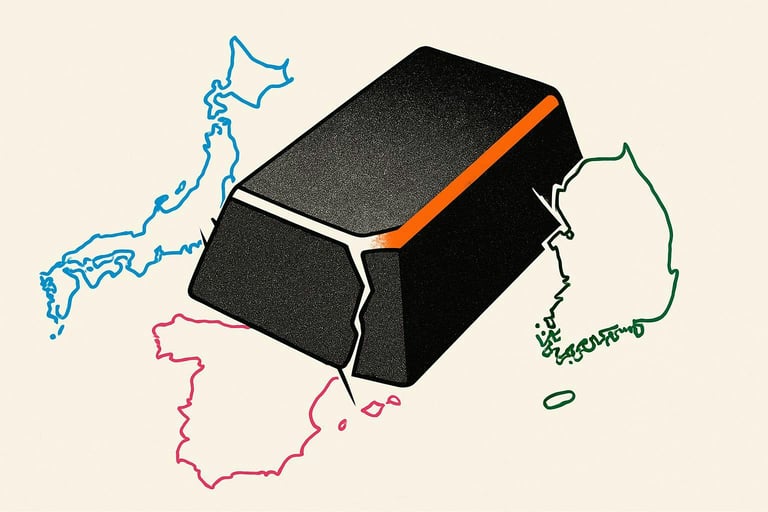

The situation has prompted a rare joint statement from Japan, Spain, and South Korea, expressing concern over falling TC/RCs and warning that the current environment hampers sustainable copper smelting and increases reliance on specific countries.

Major Japanese smelters like JX Advanced Metals and Mitsubishi Materials are scaling back operations due to margin erosion, illustrating the immediate operational impacts of the fee crisis.

Industry responses include diversification, strategic government collaborations, and operational efficiencies, with opportunities for facilities that can innovate and align with national security and supply chain priorities.

Policymakers and industry leaders are urged to strengthen supply-chain resilience and promote international cooperation to prevent future bottlenecks in critical resources.

The crisis underscores the importance of supply chain diversification and strategic planning, emphasizing the need for balanced regional capacities and long-term partnerships to ensure market stability.

Industry experts predict the market will remain tight into 2026, with Chinese policy interventions possibly occurring over the next five years to help rebalance supply.

Long-term contracts and byproduct revenues from sulfuric acid and precious metals help buffer short-term volatility, but reliance on volatile markets poses long-term profitability risks.

The supply-demand imbalance is further aggravated by a concentrate supply deficit, which is expected to tighten inventories and push prices higher, complicating the market outlook.

Future industry restructuring will likely involve regional specialization, consolidation, and diversification into critical metals and strategic partnerships, moving beyond traditional treatment charge models.

The industry warns that the current market environment hampers sustainable development and increases dependence on specific nations, raising geopolitical and supply chain risks.

Summary based on 5 sources

Get a daily email with more Macroeconomics stories

Sources

Investing.com • Oct 15, 2025

Japan, Spain, South Korea warn over unsustainable copper processing fees

NewsX • Oct 15, 2025

Japan, Spain, South Korea warn over unsustainable copper processing fees

Finimize • Oct 15, 2025

Copper’s Squeeze Leaves Smelters And Miners Feeling The Heat

Discovery Alert • Oct 15, 2025

Global Copper Smelters Market Challenges Threaten Industry Viability in 2025